7 Heteroskedasticity

Learning outcomes

By the end of this chapter the reader should be able to:

- State the homoskedasticity assumption MLR.5 in Wooldridge’s notation and recognise when it is likely to fail in cross-sectional data.

- Explain why heteroskedasticity leaves OLS unbiased and consistent but destroys efficiency and invalidates the usual standard errors, \(t\)-tests, and \(F\)-tests.

- Detect heteroskedasticity informally with residual plots and formally with the Goldfeld–Quandt and Breusch–Pagan tests.

- Correct heteroskedasticity by Weighted Least Squares (WLS) when the form of the conditional variance is known.

- Compute and report heteroskedasticity-robust (White / HC1) standard errors when the form is unknown.

- Build a side-by-side table comparing OLS standard errors with robust standard errors and interpret the ratio.

Motivating empirical question

Why do conventional OLS confidence intervals understate the true uncertainty in a wage regression with very dispersed top earners — and what should we do about it?

A regression of hourly wages on years of education delivers a clean point estimate of the return to schooling. But the spread of wages around the regression line is not the same for high-school dropouts and for PhDs: graduates fan out across a much wider range of salaries. The textbook OLS formula for the standard error of \(\hat\beta_1\) assumes the spread is constant. When it is not, the reported standard errors are wrong, the \(t\)-statistics are wrong, and the policy recommendations built on them are wrong. This chapter shows how to diagnose the problem and how to fix it.

A separation of concerns up front: this chapter is about inference given identification, not about identification itself. OLS coefficient estimates remain meaningful as estimates of conditional means even when standard errors are wrong; we fix the standard errors here, not the causal question. The “correlation is not causation” thread from Chapters 1–5 still applies — nothing in this chapter rescues a regression with omitted-variable bias. We are repairing the inferential machinery on top of OLS, not the OLS slope itself.

7.1 Introduction

Chapter 4 we listed the multiple linear regression assumptions MLR.1–MLR.6 that justify OLS. The homoskedasticity assumption MLR.5 states that the error variance is the same for every value of the regressors:

\[ \operatorname{Var}(u_i \mid \mathbf{x}_i) \;=\; \sigma^2, \qquad i = 1, \dots, n. \]

When MLR.5 fails, the conditional variance depends on \(\mathbf{x}_i\):

\[ \operatorname{Var}(u_i \mid \mathbf{x}_i) \;=\; \sigma_i^2, \]

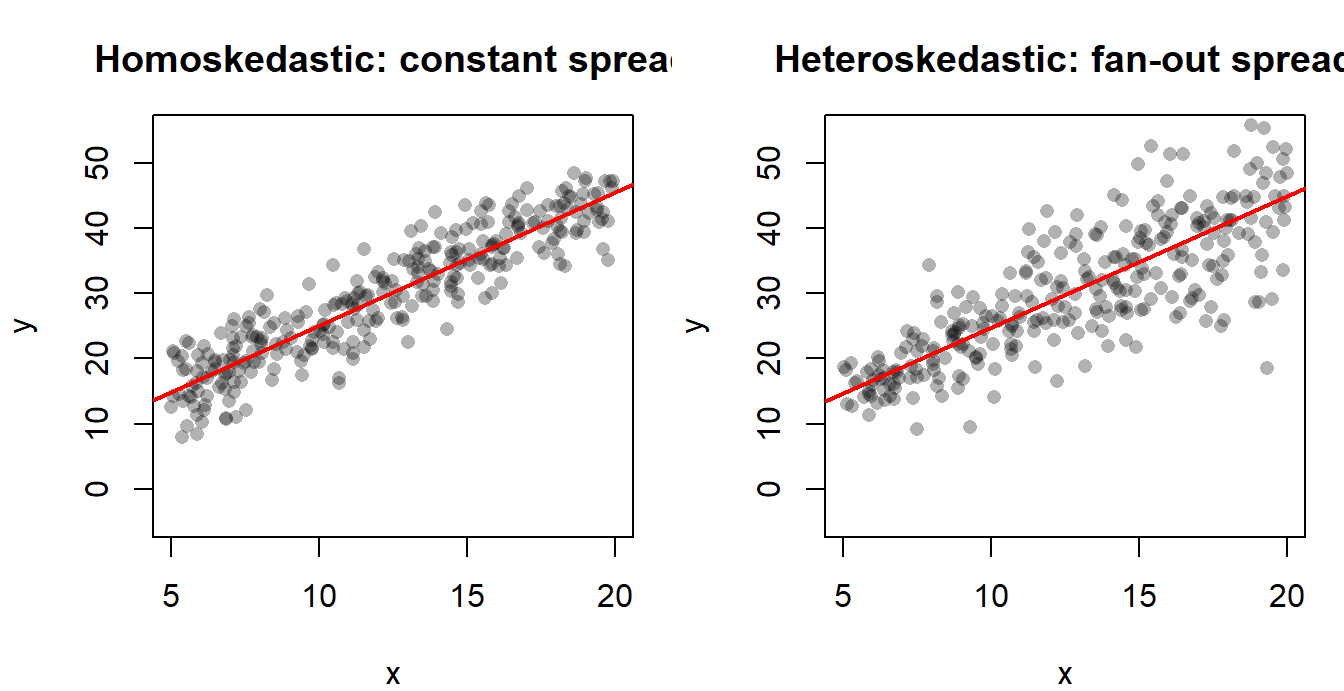

and the error is said to be heteroskedastic. The Greek root is helpful: homo-skedastic means “same spread”; hetero-skedastic means “different spread”.

NoteExample: wage variability and education

Workers with only primary education in a typical European labour market earn between roughly 15{,}000 and 25{,}000 euros per year — a narrow range. University graduates earn anywhere from 20{,}000 to 200{,}000 euros — a much wider range. The conditional variance of wages clearly increases with education. The error term in a wage equation \(\text{wage}_i = \beta_0 + \beta_1\,\text{educ}_i + u_i\) therefore exhibits heteroskedasticity: \(\operatorname{Var}(u_i \mid \text{educ}_i)\) grows with educ.

Heteroskedasticity is not a problem of identification. As long as \(\mathbb{E}[u_i \mid \mathbf{x}_i] = 0\) (assumption MLR.4) holds, the meaning of \(\beta_j\) as a ceteris paribus effect survives. What heteroskedasticity breaks is inference — the machinery that turns a point estimate \(\hat\beta_j\) into a confidence interval or a hypothesis test.

WarningCommon mistake: confusing heteroskedasticity with omitted variable bias

Heteroskedasticity is about \(\operatorname{Var}(u_i \mid \mathbf{x}_i)\); omitted variable bias is about \(\mathbb{E}[u_i \mid \mathbf{x}_i]\). The first leaves \(\hat\beta_j\) unbiased and only damages the standard errors. The second biases \(\hat\beta_j\) itself. The two problems require different tools, and the same dataset can suffer from one, the other, both, or neither.

NoteWhere heteroskedasticity typically appears

Heteroskedasticity is the rule rather than the exception in cross-sectional microeconomic data, for at least three reasons:

- Scale effects. Larger units have more room to vary. Spending by large firms varies more in absolute terms than spending by small firms.

- Discrete and bounded outcomes. A binary dependent variable mechanically has \(\operatorname{Var}(y \mid \mathbf{x}) = p(\mathbf{x})\bigl[1 - p(\mathbf{x})\bigr]\), which is not constant.

- Aggregation. Means computed over groups of different sizes have variances proportional to \(1/n_g\), generating heteroskedasticity by construction.

These are precisely the data structures applied economists work with, which is why robust standard errors have become the default in modern practice.

7.2 Consequences of heteroskedasticity

Assume MLR.1–MLR.4 hold and only MLR.5 fails. Three statements summarise the consequences:

- OLS is still unbiased and consistent. Unbiasedness of \(\hat\beta_j\) requires only MLR.1–MLR.4. Heteroskedasticity does not enter the proof.

- OLS is no longer BLUE. The Gauss–Markov theorem requires homoskedasticity. Under heteroskedasticity, other linear unbiased estimators can have a smaller variance than OLS. We will see one such estimator, WLS, in §7.4.

- The usual OLS standard errors are wrong. The textbook formula \(\widehat{\operatorname{Var}}(\hat\beta_j) = \hat\sigma^2 (\mathbf{X}'\mathbf{X})^{-1}_{jj}\) assumes the error variance-covariance matrix is \(\sigma^2 \mathbf{I}_n\). When it is not, this formula is biased. In the most common case — variance that increases with the regressors, the typical “fan” shape illustrated above — OLS standard errors are too small and \(t\)-statistics too large, so confidence intervals are too narrow and we reject the null more often than we should. The opposite direction is possible too: when high-variance observations happen to have low leverage on the slope, robust standard errors can come out smaller than OLS. This is less common in practice but worth knowing so the diagnosis is “the OLS formula is wrong” rather than “the OLS formula is always optimistic”.

NoteThe correct (sandwich) variance under heteroskedasticity

If we collect the conditional variances on the diagonal of a matrix \(\Omega = \operatorname{diag}(\sigma_1^2, \dots, \sigma_n^2)\), the correct conditional variance of the OLS estimator is

\[ \operatorname{Var}(\hat{\beta} \mid \mathbf{X}) \;=\; (\mathbf{X}'\mathbf{X})^{-1}\,\mathbf{X}'\Omega\mathbf{X}\,(\mathbf{X}'\mathbf{X})^{-1}. \]

The “bread” \((\mathbf{X}'\mathbf{X})^{-1}\) surrounds the “meat” \(\mathbf{X}'\Omega\mathbf{X}\) — which is why this form is universally called a sandwich estimator. The usual OLS formula simply replaces \(\Omega\) by \(\sigma^2 \mathbf{I}_n\) and collapses the sandwich to a single slice. The White / HC1 estimator we use in §7.4 estimates \(\Omega\) by \(\operatorname{diag}(\hat u_1^2, \dots, \hat u_n^2)\), with a small-sample degrees-of-freedom correction.

In short: heteroskedasticity is a standard-error problem, not a coefficient problem. The fix is to repair the inferential machinery (robust SEs) or, if we can afford the extra modelling, to use an estimator that exploits the variance structure (WLS).

7.3 Detection of heteroskedasticity

We describe one informal diagnostic and two formal tests. The informal plot is cheap and should be the first thing you look at; the formal tests give a structured decision rule.

7.3.1 Informal detection: residual plots

After estimating the OLS model, compute the residuals \(\hat u_i = y_i - \hat y_i\) and plot them against either the fitted values \(\hat y_i\) or against each regressor \(x_j\). The visual fingerprint of heteroskedasticity is a fan or wedge shape: the vertical spread of the residual cloud widens (or narrows) as you move along the horizontal axis. Squared residuals \(\hat u_i^2\) against \(x_j\) make the pattern even more obvious because the sign of the residual no longer matters.

If the cloud looks like a horizontal band of roughly constant thickness, homoskedasticity is plausible. If it spreads out — as it typically does when \(x_j\) is income, firm size, or any other “scale” variable — heteroskedasticity is the natural suspect.

7.3.2 The Goldfeld–Quandt test

The Goldfeld–Quandt (GQ) test is appropriate when you suspect heteroskedasticity is driven by one specific regressor. The idea is simple: split the sample into a low-\(x\) group and a high-\(x\) group and compare the residual variances of the two subsamples.

Steps.

- Order the observations by the suspected variable \(x\).

- Optionally drop the middle \(m\) observations (often \(m \approx n/3\)) to accentuate the contrast.

- Estimate the model separately on the low group (subsample 1) and on the high group (subsample 2). Obtain the sums of squared residuals \(\operatorname{SSR}_1\) and \(\operatorname{SSR}_2\), with degrees of freedom \(\operatorname{df}_1\) and \(\operatorname{df}_2\).

- Compute

\[ F \;=\; \frac{\operatorname{SSR}_2 \,/\, \operatorname{df}_2}{\operatorname{SSR}_1 \,/\, \operatorname{df}_1}\;\sim\;F_{\operatorname{df}_2,\,\operatorname{df}_1} \quad \text{under } H_0. \]

Hypotheses. \(H_0\): homoskedasticity. \(H_1\): \(\operatorname{Var}(u)\) increases with \(x\) (the most common alternative). Reject \(H_0\) when \(F\) exceeds the upper-tail critical value of the \(F\) distribution.

The GQ test was historically popular in small samples and is intuitive, but it requires the analyst to commit to a single sorting variable and to a sample-splitting rule. The Breusch–Pagan test, introduced next, drops both of these commitments.

7.3.3 The Breusch–Pagan test

Start from the picture, not the formula. If heteroskedasticity exists, then \(\operatorname{Var}(u_i \mid \mathbf{x}_i)\) moves with \(\mathbf{x}_i\) — and because the squared residual \(\hat u_i^2\) is our sample window onto the unobserved \(u_i^2\), large squared residuals should cluster at certain values of \(\mathbf{x}\) rather than scatter evenly. So the natural diagnostic is: regress \(\hat u_i^2\) on \(\mathbf{x}_i\) and see if anything explains it. If the regressors explain a non-trivial share of the variation in \(\hat u_i^2\), then \(\operatorname{Var}(u \mid \mathbf{x})\) depends on \(\mathbf{x}\) — which is the definition of heteroskedasticity. If they explain essentially nothing, the squared residuals look like noise around a constant, and homoskedasticity is plausible.

That is the whole Breusch–Pagan (BP) idea. Unlike Goldfeld–Quandt, it detects heteroskedasticity related to any of the regressors, without committing to a single sorting variable. It is the workhorse formal test in modern applied work, and the test statistic below is just a way of asking “is the auxiliary \(R^2\) large enough to take seriously?”

Steps.

- Estimate the original model by OLS and store the residuals \(\hat u_i\).

- Run the auxiliary regression of the squared residuals on all the original regressors:

\[ \hat u_i^2 \;=\; \gamma_0 + \gamma_1 x_{1i} + \gamma_2 x_{2i} + \dots + \gamma_k x_{ki} + v_i. \]

- Compute the BP statistic

\[ \operatorname{BP} \;=\; n \cdot R^2_{\text{aux}} \;\sim\;\chi^2_{k}\quad\text{under } H_0, \]

where \(R^2_{\text{aux}}\) is the coefficient of determination of the auxiliary regression and \(k\) is the number of slope coefficients in it.

Hypotheses. \(H_0: \gamma_1 = \gamma_2 = \dots = \gamma_k = 0\) (homoskedasticity). Reject when \(\operatorname{BP} > \chi^2_{k,\alpha}\).

A close cousin — the White test — adds squares and cross-products of the regressors to the auxiliary regression and so detects more general forms of heteroskedasticity, at the cost of degrees of freedom.

WarningCommon mistake: chaining tests until one rejects

Do not run GQ, then BP, then White, and report whichever rejects “first”. This is a form of \(p\)-hacking. Pick one test based on what you suspect before looking at the residuals, or — following modern practice — skip the testing step altogether and report robust standard errors by default.

7.4 Remedies

There are two main remedies, suited to two different states of knowledge.

7.4.1 Weighted Least Squares (WLS)

Suppose we know (or are willing to model) the form of the conditional variance:

\[ \operatorname{Var}(u_i \mid \mathbf{x}_i) \;=\; \sigma^2 \, h(\mathbf{x}_i), \]

where \(h(\mathbf{x}_i) > 0\) is a known function of the regressors. A typical example is \(h(\mathbf{x}_i) = x_i\) when the variance is proportional to a scale variable such as income.

Divide every term in the regression by \(\sqrt{h(\mathbf{x}_i)}\):

\[ \frac{y_i}{\sqrt{h(\mathbf{x}_i)}} \;=\; \beta_0 \frac{1}{\sqrt{h(\mathbf{x}_i)}} + \beta_1 \frac{x_{i}}{\sqrt{h(\mathbf{x}_i)}} + \frac{u_i}{\sqrt{h(\mathbf{x}_i)}}. \]

The new error \(u_i^\ast = u_i / \sqrt{h(\mathbf{x}_i)}\) has constant variance:

\[ \operatorname{Var}(u_i^\ast) \;=\; \frac{\sigma^2 h(\mathbf{x}_i)}{h(\mathbf{x}_i)} \;=\; \sigma^2. \]

OLS on the transformed model is equivalent to weighted least squares: minimise

\[ \sum_{i=1}^{n} \frac{1}{h(\mathbf{x}_i)} \bigl(y_i - \beta_0 - \beta_1 x_{i} - \dots\bigr)^2. \]

Each observation receives weight \(w_i = 1 / h(\mathbf{x}_i)\). Observations with high variance receive less weight; observations with low variance receive more. When the weights are correctly specified, WLS is BLUE: it has lower variance than OLS while remaining unbiased.

WarningCommon mistake: forcing WLS when you don’t know \(h(\mathbf{x})\)

WLS is only BLUE under correctly specified weights. With wrong weights it can be less efficient than OLS, and its standard errors are again incorrect. If you have only a vague idea of the variance structure, prefer robust standard errors.

7.4.2 Heteroskedasticity-robust standard errors

When the form of \(h(\mathbf{x})\) is unknown, the safer remedy is to keep OLS for the point estimates and to compute heteroskedasticity-consistent (HC) standard errors, also called robust or White standard errors after (White 1980).

In the simple regression case with \(\hat u_i\) denoting the OLS residual,

\[ \operatorname{se}_{\text{robust}}(\hat\beta_1) \;=\; \sqrt{\,\dfrac{\displaystyle\sum_{i=1}^{n} (x_i - \bar x)^2 \,\hat u_i^2}{\Bigl[\displaystyle\sum_{i=1}^{n} (x_i - \bar x)^2\Bigr]^2}\,}. \]

The general matrix expression is the sandwich estimator of §7.2 with \(\Omega\) replaced by \(\operatorname{diag}(\hat u_1^2, \dots, \hat u_n^2)\). Several variants exist (HC0, HC1, HC2, HC3) that differ in their finite-sample degrees-of-freedom correction; HC1 is the default reported by Stata’s , robust option and is the standard in published applied work.

Robust SEs leave the point estimates \(\hat\beta_j\) unchanged. Only the variance — and therefore the \(t\)-statistics, \(p\)-values, and confidence intervals — is corrected.

NoteWhen to use what

- Variance structure known and trustworthy \(\Rightarrow\) WLS (BLUE, smaller SEs).

- Variance structure unknown \(\Rightarrow\) OLS with robust SEs (unbiased coefficients, valid inference, larger SEs).

- In doubt \(\Rightarrow\) report robust SEs. In modern applied econometrics, robust SEs have become the default rather than a backup. Many journals expect them by construction.

7.5 Lab: heteroskedasticity

This lab follows Tutorial 8 of the course. The dataset het_data.xlsx is a custom cross-section of household-level consumption and income, divided into three income groups (group \(\in \{1, 2, 3\}\), low to high). We fit a simple Engel-curve-style regression of consumption on income, detect heteroskedasticity, and then fix it twice — first by WLS and then by robust standard errors.

We use three packages: readxl to read the Excel file, lmtest for the Breusch–Pagan and Goldfeld–Quandt tests and for coeftest(), and sandwich for the robust variance–covariance matrix.

Code

library(readxl)

library(lmtest)

library(sandwich)7.5.1 Loading the data

The original tutorial uses a relative path (read_excel("het_data.xlsx")) after running setwd() into the Tutorial 8 folder. For portability in this book we keep that style but document the absolute path used at compile time. Adapt the path to your machine.

Code

het_path <- file.path(

"..", "..", "..", "Practicas", "2025", "Tutorial 8", "het_data.xlsx"

)

het_data <- read_excel(het_path)

# Construct a tercile-of-income indicator for the Goldfeld-Quandt split:

# group == 1 = low-income third, 2 = middle third, 3 = high-income third.

het_data$group <- as.integer(cut(het_data$income,

breaks = quantile(het_data$income,

probs = c(0, 1/3, 2/3, 1)),

include.lowest = TRUE))

str(het_data)tibble [30 × 4] (S3: tbl_df/tbl/data.frame)

$ id : num [1:30] 1 2 3 4 5 6 7 8 9 10 ...

$ consumption: num [1:30] 433 663 690 727 800 ...

$ income : num [1:30] 649 939 956 1067 1071 ...

$ group : int [1:30] 1 1 1 1 1 1 1 1 1 1 ...Code

head(het_data)# A tibble: 6 × 4

id consumption income group

<dbl> <dbl> <dbl> <int>

1 1 433. 649. 1

2 2 663. 939. 1

3 3 690. 956. 1

4 4 727. 1067. 1

5 5 800. 1071. 1

6 6 777. 1215. 1The original xlsx ships with income and consumption. We add a derived group variable equal to the income tercile (1 = low, 2 = middle, 3 = high) so the Goldfeld–Quandt test below can subset the sample.

7.5.2 Step 1. OLS baseline and residual plot

Code

model1 <- lm(consumption ~ income, data = het_data)

summary(model1)

Call:

lm(formula = consumption ~ income, data = het_data)

Residuals:

Min 1Q Median 3Q Max

-280.684 -52.408 2.257 58.517 234.525

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 13.94848 70.77718 0.197 0.845

income 0.65532 0.03864 16.961 2.91e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 117.5 on 28 degrees of freedom

Multiple R-squared: 0.9113, Adjusted R-squared: 0.9081

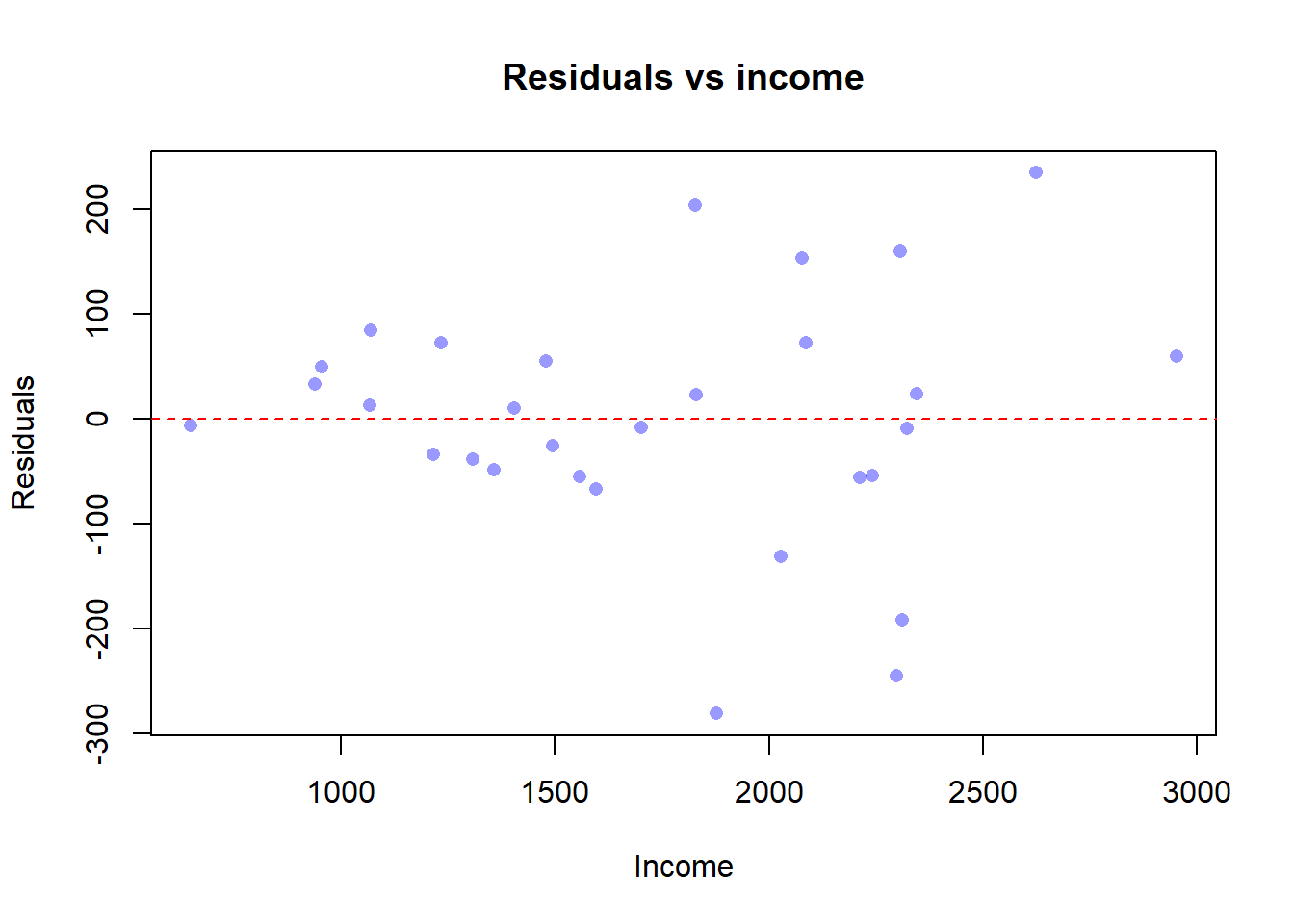

F-statistic: 287.7 on 1 and 28 DF, p-value: 2.91e-16The slope \(\hat\beta_1\) is the average marginal propensity to consume out of income. To check homoskedasticity informally, plot the OLS residuals against income:

Code

plot(het_data$income, resid(model1),

xlab = "Income",

ylab = "Residuals",

main = "Residuals vs income",

pch = 16,

col = rgb(0, 0, 1, 0.4))

abline(h = 0, lty = 2, col = "red")

The cloud opens up as income grows: the residuals fan out. This is exactly the wedge shape we warned about in §7.3.1.

7.5.3 Step 2. Goldfeld–Quandt test by hand

Estimate the model separately on the low-income (group == 1) and high-income (group == 3) subsamples, then compare the two residual variances.

Code

model_low <- lm(consumption ~ income, data = het_data, subset = group == 1)

model_high <- lm(consumption ~ income, data = het_data, subset = group == 3)

SSR_low <- sum(residuals(model_low)^2)

SSR_high <- sum(residuals(model_high)^2)

n_low <- nobs(model_low)

n_high <- nobs(model_high)

k <- length(coef(model_low)) # intercept + slope

df_low <- n_low - k

df_high <- n_high - k

F_gq <- (SSR_high / df_high) / (SSR_low / df_low)

F_crit <- qf(0.95, df_high, df_low)

p_gq <- 1 - pf(F_gq, df_high, df_low)

c(F = F_gq, F_crit_5pct = F_crit, p_value = p_gq) F F_crit_5pct p_value

9.582976952 3.438101233 0.002205927 If F_gq is well above F_crit_5pct — equivalently, if the \(p\)-value is below \(0.05\) — we reject homoskedasticity in favour of “variance increases with income”.

7.5.4 Step 3. Breusch–Pagan test (by hand and with bptest())

The auxiliary regression of squared residuals on income gives us \(R^2_{\text{aux}}\); the BP statistic is \(n \cdot R^2_{\text{aux}}\) and follows a \(\chi^2_1\) under \(H_0\) (we have one regressor, income).

Code

res <- residuals(model1)

res_sq <- res^2

aux <- lm(res_sq ~ income, data = het_data)

n <- nobs(model1)

R2_aux <- summary(aux)$r.squared

BP_stat <- n * R2_aux

chi_crit <- qchisq(0.95, df = 1)

p_bp <- 1 - pchisq(BP_stat, df = 1)

c(BP_manual = BP_stat, chi2_1_5pct = chi_crit, p_value = p_bp) BP_manual chi2_1_5pct p_value

4.86609184 3.84145882 0.02738946 The package version delivers the same answer in one line:

Code

bptest(model1)

studentized Breusch-Pagan test

data: model1

BP = 4.8661, df = 1, p-value = 0.02739

NoteReading the

bptest() output

bptest() prints four lines and a model line. The map to §7.3.3 is:

studentized Breusch-Pagan test→ name of the procedure.data: model1→ the OLS fit the test is being applied to.BP→ the test statistic, \(n \cdot R^2_{\text{aux}}\) from the auxiliary regression of \(\hat u_i^2\) on the regressors.df→ the degrees of freedom of the asymptotic \(\chi^2\) reference distribution; equals the number of slope regressors in the auxiliary regression (one here,income).p-value→ the right-tail probability under \(\chi^2_{\text{df}}\). Reject \(H_0\) at the 5% level when this is below 0.05.

A small \(p\)-value (below \(0.05\)) means we reject homoskedasticity. The two computations should agree up to rounding.

7.5.5 Step 4. WLS correction

Assume \(\operatorname{Var}(u_i \mid \text{income}_i) \propto \text{income}_i\), so \(h(\text{income}_i) = \text{income}_i\). The WLS weights are \(w_i = 1 / \text{income}_i\).

Code

wls <- lm(consumption ~ income, data = het_data, weights = 1 / income)

summary(wls)

Call:

lm(formula = consumption ~ income, data = het_data, weights = 1/income)

Weighted Residuals:

Min 1Q Median 3Q Max

-6.4405 -1.1894 0.0547 1.3568 4.7847

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 34.45170 55.08024 0.625 0.537

income 0.64357 0.03354 19.185 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 2.607 on 28 degrees of freedom

Multiple R-squared: 0.9293, Adjusted R-squared: 0.9268

F-statistic: 368.1 on 1 and 28 DF, p-value: < 2.2e-16To check whether the weights were well chosen, re-test for heteroskedasticity in the WLS fit:

Code

bptest(wls)

studentized Breusch-Pagan test

data: wls

BP = 0.0056423, df = 1, p-value = 0.9401If the BP test no longer rejects (large \(p\)-value), the assumed variance structure was approximately correct and WLS has done its job.

7.5.6 Step 5. Robust (HC1) standard errors

The safer remedy — valid even when we have no idea what \(h(\mathbf{x})\) looks like — is to keep the OLS point estimates and recompute the standard errors with vcovHC():

Code

coeftest(model1, vcov = vcovHC(model1, type = "HC1"))

t test of coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 13.948477 49.970518 0.2791 0.7822

income 0.655317 0.035729 18.3411 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

NoteReading the

coeftest() output — the column journals expect

coeftest() from lmtest prints a familiar-looking coefficient table, but the Std. Error column is computed from the matrix you pass to vcov — here the HC1 sandwich estimator from vcovHC(). The map:

Estimate→ identical tosummary(model1)$coefficients[, "Estimate"]. Robust standard errors do not change point estimates.Std. Error→ the robust standard error: \(\sqrt{\bigl[(\mathbf{X}'\mathbf{X})^{-1}\,\mathbf{X}'\hat\Omega\mathbf{X}\,(\mathbf{X}'\mathbf{X})^{-1}\bigr]_{jj}}\), with \(\hat\Omega = \operatorname{diag}(\hat u_1^2, \dots, \hat u_n^2)\) scaled by the HC1 small-sample correction. This is the column most journals will ask for.t value→Estimate / Std. Error, with the robust SE in the denominator. Compare to the OLSt valuefromsummary(model1): the numerator is the same, the denominator has changed.Pr(>|t|)→ two-sided \(p\)-value computed from the same \(t\)-distribution as in §4.3; the difference from the OLS column is driven entirely by the change in the standard error.

The point estimates are identical to summary(model1). Only the standard errors, \(t\)-statistics, and \(p\)-values change.

7.5.7 Step 6. Comparison table: OLS SEs vs robust SEs

A clean way to communicate the result is to put the two standard errors side by side and report their ratio.

Code

se_ols <- summary(model1)$coefficients[, "Std. Error"]

se_robust <- sqrt(diag(vcovHC(model1, type = "HC1")))

comparison <- data.frame(

OLS_SE = round(se_ols, 4),

Robust_SE = round(se_robust, 4),

Ratio = round(se_robust / se_ols, 3)

)

comparison OLS_SE Robust_SE Ratio

(Intercept) 70.7772 49.9705 0.706

income 0.0386 0.0357 0.925If the ratio in the last column is materially larger than \(1\), the OLS standard errors were understating uncertainty — exactly the diagnosis we made in §7.2.

NoteReading the comparison table

The point of this table is not to “choose” one column over the other — the coefficients are the same in both columns. The table tells you how much the OLS standard error has been distorted by heteroskedasticity. A ratio close to \(1.0\) means OLS was fine even though MLR.5 technically failed; a ratio above \(1.5\) means OLS would have led you to over-reject the null. Either way, robust SEs are now the standard column to report.

Self-check

Six short multiple-choice questions. Try each one before opening the answer.

TipQ1. Definition

Heteroskedasticity in a linear regression model means:

- A. \(\mathbb{E}[u \mid x] \neq 0\).

- B. \(\operatorname{Var}(u \mid x)\) depends on \(x\) — it is not constant.

- C. The error \(u\) is correlated across observations.

- D. \(x\) is collinear with another regressor.

Answer: B. Heteroskedasticity is, by definition, a failure of MLR.5: the conditional variance of \(u\) varies with the regressors. The other options describe MLR.4, autocorrelation, and multicollinearity respectively.

TipQ2. Consequences

Under heteroskedasticity (with MLR.1–MLR.4 still holding), OLS is:

- A. Biased in finite samples.

- B. Inconsistent.

- C. Still unbiased and consistent, but no longer BLUE, and the usual standard errors are wrong.

- D. Still BLUE.

Answer: C. Unbiasedness and consistency of \(\hat\beta_j\) do not require MLR.5. Efficiency (BLUE) and the validity of the textbook standard error formula do.

TipQ3. Identification versus inference

Why do we say heteroskedasticity is an inference problem, not an identification problem?

- A. Because heteroskedasticity biases \(\hat\beta_j\) but leaves the standard errors intact.

- B. Because \(\hat\beta_j\) is no longer consistent for the population slope.

- C. Because, if MLR.4 still holds, \(\hat\beta_j\) still estimates the ceteris paribus effect; only the standard errors are wrong.

- D. Because heteroskedasticity is the same thing as omitted variable bias.

Answer: C. The causal interpretation of \(\hat\beta_j\) survives heteroskedasticity. What fails is the machinery that turns the estimate into a \(t\)-test or a confidence interval.

TipQ4. Breusch–Pagan

The Breusch–Pagan test runs an auxiliary regression of:

- A. \(\hat u\) on the regressors and uses the resulting \(F\) statistic.

- B. \(\hat u^2\) on the regressors and uses \(n \cdot R^2\) as a \(\chi^2\) statistic.

- C. \(y\) on \(\hat u^2\) and uses a \(t\) statistic.

- D. \(x\) on \(\hat u\) and uses the slope as a test statistic.

Answer: B. The BP test regresses the squared residuals on the regressors; under \(H_0\) of homoskedasticity, \(n R^2_{\text{aux}}\) is asymptotically \(\chi^2_k\).

TipQ5. Goldfeld–Quandt

The Goldfeld–Quandt test compares:

- A. The two estimated slopes.

- B. The residual variances of two subsamples (typically low vs high values of a regressor).

- C. The \(R^2\) of two models.

- D. Two intercepts.

Answer: B. GQ splits the sample by the suspected variable, fits the regression on each half, and uses the ratio of mean squared residuals as an \(F\) statistic.

TipQ6. WLS versus robust SEs

When should you prefer Weighted Least Squares to OLS with robust standard errors?

- A. When the form of \(\operatorname{Var}(u \mid \mathbf{x})\) is correctly known and you want efficiency gains.

- B. Whenever the Breusch–Pagan test rejects, regardless of what you know.

- C. When the sample is small and you cannot compute robust SEs.

- D. Never — robust SEs always dominate WLS.

Answer: A. WLS is BLUE only under correctly specified weights. With unknown variance structure, OLS plus robust SEs is the safer default; with a credible model for \(h(\mathbf{x})\), WLS buys efficiency.

Exercises

Exercise 7.1 ★ — Spotting heteroskedasticity. For each of the following regressions, predict whether the error term is likely to be heteroskedastic and explain why in one sentence.

- Annual food expenditure regressed on household income across a sample of 4{,}000 households.

- Number of children regressed on mother’s age, in a sample restricted to women aged 30–35.

- Firm-level R&D spending regressed on firm sales in a sample mixing small startups and Fortune 500 companies.

- A linear-probability model where the dependent variable is a \(0/1\) indicator for employment.

TipShow answer

- Yes — richer households have more discretionary spending and therefore wider absolute variation in food spending. (b) Probably not strongly — the sample is narrow in age, so scale effects are small. (c) Yes, severely — firm size spans several orders of magnitude. (d) Yes, by construction — \(\operatorname{Var}(y \mid \mathbf{x}) = p(\mathbf{x})\bigl[1-p(\mathbf{x})\bigr]\) depends on \(\mathbf{x}\) whenever \(p(\mathbf{x})\) does.

Exercise 7.2 ★ — Reading a BP output. A student runs bptest(lm(consumption ~ income, data = het_data)) and obtains a test statistic of about \(9.8\) on \(1\) degree of freedom, with \(p\)-value \(\approx 0.002\).

- State the null and alternative hypotheses of the test.

- What is the conclusion at the \(5\%\) level?

- Should the student now (i) keep OLS standard errors, (ii) switch to robust standard errors, or (iii) re-estimate by WLS? Justify briefly.

TipShow answer

- \(H_0\): homoskedasticity (\(\gamma_1 = 0\) in the auxiliary regression of \(\hat u^2\) on income); \(H_1\): \(\operatorname{Var}(u \mid \text{income})\) depends on income. (b) Reject \(H_0\) at the \(5\%\) level: the \(p\)-value is well below \(0.05\). (c) At minimum, switch to robust SEs (option ii). WLS (option iii) is an option if the student is confident the variance is proportional to income; otherwise the robust route is safer.

Exercise 7.3 ★★ — Goldfeld–Quandt by hand. Suppose for a regression of consumption on income you obtain \(\operatorname{SSR}_{\text{low}} = 120\) on \(\operatorname{df}_{\text{low}} = 28\) observations in the low-income subsample, and \(\operatorname{SSR}_{\text{high}} = 540\) on \(\operatorname{df}_{\text{high}} = 28\) in the high-income subsample. The \(5\%\) critical value of \(F_{28,28}\) is approximately \(1.88\).

- Compute the Goldfeld–Quandt \(F\) statistic.

- State your conclusion at the \(5\%\) level.

- What economic story would explain a result of this kind?

A full answer is given in the Instructor Edition.

Exercise 7.4 ★★ — Why the sandwich. Show that under homoskedasticity (\(\Omega = \sigma^2 \mathbf{I}_n\)), the sandwich variance

\[ (\mathbf{X}'\mathbf{X})^{-1}\mathbf{X}'\Omega\mathbf{X}(\mathbf{X}'\mathbf{X})^{-1} \]

reduces to the usual OLS variance \(\sigma^2(\mathbf{X}'\mathbf{X})^{-1}\). Use this to argue, in one paragraph, that the robust standard error is never worse asymptotically than the OLS standard error.

A full answer is given in the Instructor Edition.

Exercise 7.5 ★★ — WLS as transformed OLS. Take the SLR model \(y_i = \beta_0 + \beta_1 x_i + u_i\) with \(\operatorname{Var}(u_i \mid x_i) = \sigma^2 x_i\) (so \(x_i > 0\)).

- Write the transformed model after dividing by \(\sqrt{x_i}\).

- Show that the error of the transformed model has constant variance equal to \(\sigma^2\).

- Conclude that OLS on the transformed model is BLUE for \((\beta_0, \beta_1)\), and write down the equivalent WLS criterion in terms of weights \(w_i\).

A full answer is given in the Instructor Edition.

Exercise 7.6 ★★★ — Lab extension. Using het_data.xlsx from Tutorial 8:

- Reproduce the comparison table of OLS standard errors and HC1 robust standard errors. Report the ratio for the slope on

income. - Re-fit the model using WLS with weights \(w_i = 1/\text{income}_i^2\) (variance proportional to \(\text{income}^2\) rather than \(\text{income}\)). Run the BP test on the resulting WLS fit. Does this second weighting scheme outperform the \(w_i = 1/\text{income}_i\) scheme of §7.5?

- Suppose the BP test still rejects after WLS. Which of the two remedies — WLS or robust SEs — should you trust more, and why?

A full answer is given in the Instructor Edition.

White, Halbert. 1980. “A Heteroskedasticity-Consistent Covariance Matrix Estimator and a Direct Test for Heteroskedasticity.” Econometrica 48 (4): 817–38. https://doi.org/10.2307/1912934.